Current Interest Rates in February 2026: Trends, Analysis, and What It Means for You

As we navigate through February 2026, interest rates—particularly mortgage rates—continue to capture attention amid economic shifts. Drawing from reliable financial sources like Freddie Mac, Zillow, the Federal Reserve, and major forecasts, this post analyzes the latest data on mortgage rates, broader interest rate trends, influencing factors, and practical advice for borrowers. With rates hovering near multi-year lows, now could be an opportune time for homebuyers, refinancers, or anyone monitoring their finances.

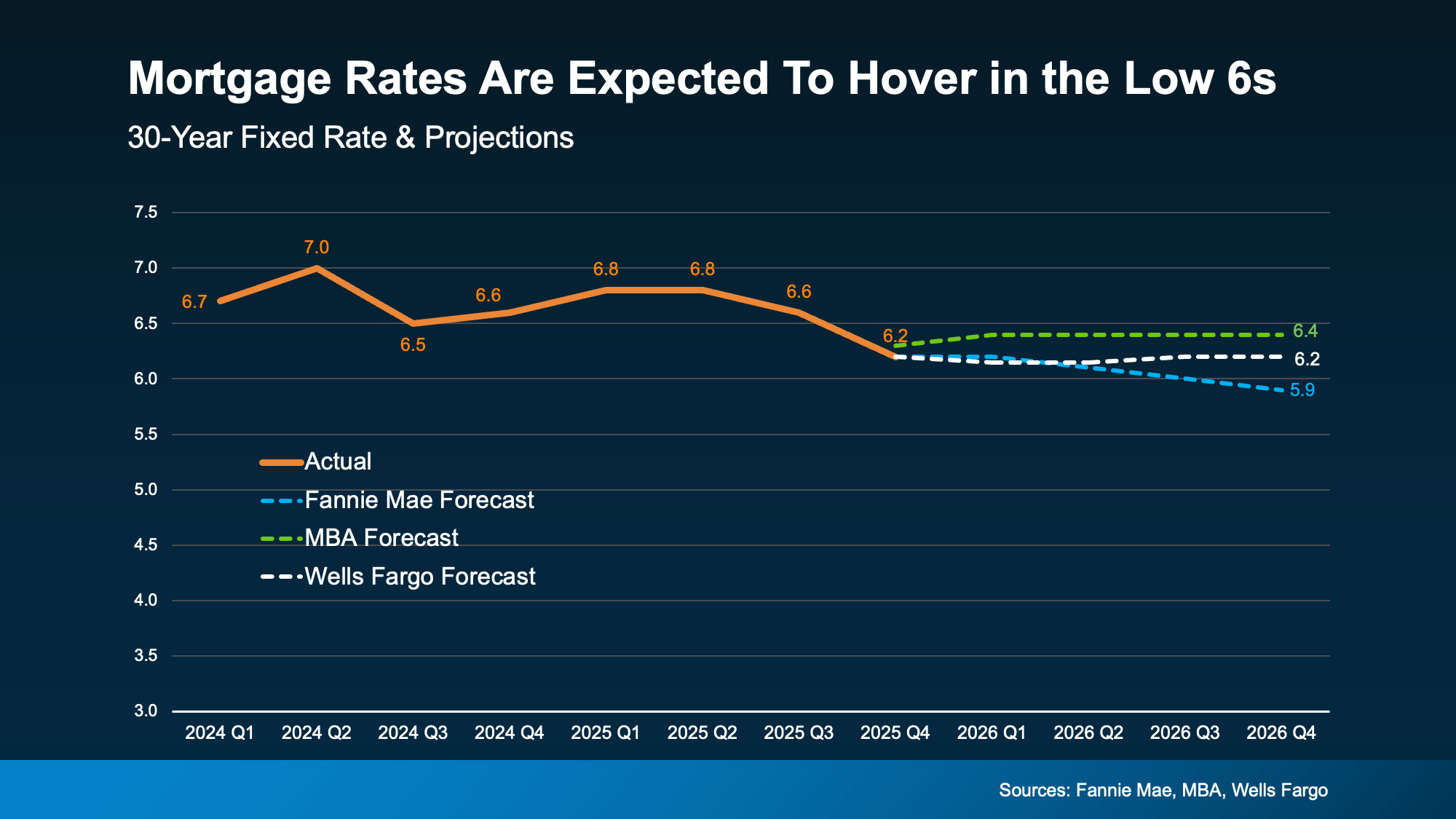

Overview of Current Mortgage Rates

Mortgage rates have stabilized in the low 6% range for 30-year fixed loans, marking a significant decline from peaks above 7% in recent years. According to Freddie Mac's weekly survey, the average 30-year fixed rate stands at 6.01%, down slightly from prior weeks and the lowest since late 2022. Zillow reports similar figures around 5.89% for purchases.

| Loan Type | Average Rate (Purchase) | Average APR (Purchase) | Average Rate (Refinance) | Source Notes |

|---|---|---|---|---|

| 30-Year Fixed | 6.01% – 6.19% | 6.19% – 6.36% | 6.22% – 6.50% | Freddie Mac (6.01%), Bankrate, WSJ, NerdWallet, Zillow |

| 15-Year Fixed | 5.35% – 5.58% | 5.39% – 5.85% | 5.44% – 5.85% | Freddie Mac (5.35%), Bankrate, CBS News, NerdWallet |

| 5/1 ARM | 5.36% – 5.99% | 5.88% – 6.31% | 5.70% – 6.28% | WSJ, Zillow, NerdWallet |

| 30-Year Jumbo | 6.16% – 6.27% | 6.25% – 6.40% | 6.25% – 6.54% | Bankrate, Investopedia |

| 30-Year VA | 5.38% – 5.71% | 5.65% – 6.16% | 5.46% – 5.66% | Zillow, Investopedia |

These rates assume good credit (700–760+ FICO), 20% down payment, and no points. Actual rates vary by lender and borrower profile.

Trends and Analysis

Mortgage rates have trended downward since mid-2025, reaching three- to four-year lows in February 2026. Forecasts from Fannie Mae, MBA, and others suggest rates will hover around 6% throughout 2026, with gradual declines possible if inflation continues easing toward the Fed’s 2% target.

This cooling has improved affordability: On a median-priced home (~$396,800) with 20% down at ~6.09%, monthly principal & interest payments are about $1,922. Refinance activity has surged as homeowners with higher rates seek relief.

Factors Influencing Interest Rates

- Economic Indicators: Rates track the 10-year Treasury yield (~4.1%), driven by inflation (2.4%), jobs data, and Fed policy.

- Federal Reserve Actions: Benchmark rate steady; potential cuts later in 2026 if data supports.

- Borrower-Specific: Credit score, down payment size, debt-to-income ratio, and loan type (VA often lowest).

Practical Advice for Borrowers

- Shop Around: Get quotes from 3–4 lenders to potentially save hundreds annually.

- Improve Your Profile: Boost credit, reduce debt, consider buying points.

- Consider Refinancing: Target at least 0.5–1% drop after closing costs.

- Choose Wisely: Fixed for stability; ARM for lower initial rate (with risk); shorter terms build equity faster.

- Use Tools: Mortgage calculators and rate trackers from Zillow, Freddie Mac, etc.

Final Thoughts

February 2026's interest rates signal a buyer-friendly environment with potential for further easing. Monitor daily fluctuations and consult a financial advisor for your situation. Rates change quickly—always verify with current lender quotes.

No comments:

Post a Comment